|

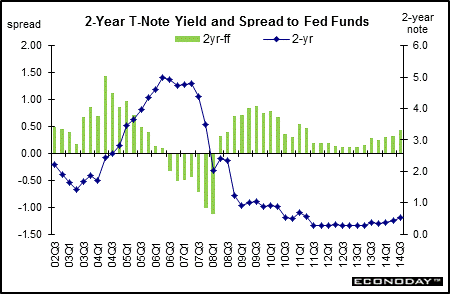

Long-term perspective Often, one can get a sense of market expectations by looking at the spread between the 2-year note yield and the fed funds rate. When the spread narrows, or even turns negative, it frequently means that market participants expect the Fed to ease monetary policy. When the spread widens, market participants are looking for tighter monetary policy. Since the start of the new millennium, the Fed has had sharp swings in policy. Early in the first decade the Fed was fighting recession and the possibility of deflation. Then the Fed went into tightening mode from mid-2004 until mid-2006. The spread fell sharply after 2004 – first as the fed funds rate rose faster than the two-year note and then during 2007 and into 2008 as the two-year-note dropped ahead of Fed rate cutting and due to flight to quality. Declines in the spread from August 2006 and into spring 2008 indicated that the markets expected lower interest rates in coming quarters. But during the remainder of 2008, the Fed cut the fed funds target so aggressively that fed funds finally fell below the 2-year T-note. More recently, the moderate-to-sluggish recovery in the U.S., recession in parts of Europe, and worries over events overseas kept the 2-year T-note yield relatively low.

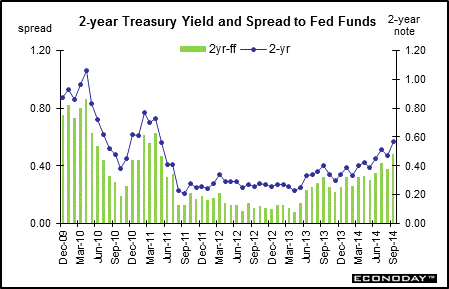

Short Term Perspective The spread between the 2-year note yield and the fed funds rate rose in June 2013 on talk of early taper by the Fed on its bond purchase programs. The 2-year spread eased in October and November after the Fed did not taper at its September 2013 policy meeting. More recently, the 2-year note has risen as the Fed has engaged in measured taper during 2014. In September, the 2-year note spread firmed 10 basis points for the month to 0.48 percent. The effective fed funds rate held steady at 0.09 percent on a monthly average basis. The effective fed funds rate is within the Fed's target range of zero to 0.25 percent. The 2-year-note yield nonetheless remains low due to expectations that the Fed will keep policy rates exceptionally low until the labor market improves significantly and inflation expectations do not exceed 2.5 percent. Also, the fed funds rate is expected to be low for a considerable period of time after taper concludes in October 2014.

|

|||||||

| Legal Notices | ©Copyright 1998-2024 Econoday, Inc. |

powered by

![[Apple App Store]](/images/AppleAppStore.png) ![[Econoday on Kindle]](/images/kindle.jpg)

|

||||||