|

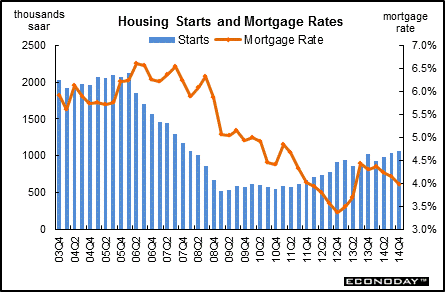

Long Term Perspective Income and interest rates are the two key factors that affect housing activity. More housing construction translates into increased demand for furniture and appliances as consumers refurnish their new homes. In the current business cycle, housing construction appears to have peaked in 2005 even as interest rates began to head higher. Starts were sharply lower in 2006 and 2007 in response to higher mortgage rates and unsold housing inventories. Tighter lending standards and the credit crunch helped push starts lower in the second half of 2007 and that trend continued into early 2009. A thawing in mortgage markets and an improved economic outlooks helped starts stabilize in 2009. Two rounds of special tax credits also boosted home sales in the summer and autumn of 2009 and spring 2010, leading to an incremental rise in starts during early 2010. During latter 2010, starts edged down on heavy supply of new homes and lackluster sales. Starts showed mild improvement in 2011 and gained moderate momentum in 2012. A gradual sell-off of housing inventory and very low mortgage rates led to modest improvement in starts in 2012 and most of 2013. Atypically adverse winter weather lowered the first quarter 2014 average although there was monthly improvement during the quarter, followed by a second quarter rebound—on average for the quarter.

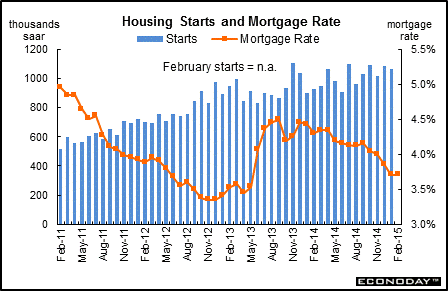

Short Term Perspective Housing starts slipped in January on weakness in single-family starts. Housing starts declined 2.0 percent in January after a 7.1 percent jump the month before. The 1.065 million unit pace was up 18.7 percent on a year-ago basis.

Single-family starts dropped 6.7 percent after a 7.9 percent boost in December. Multifamily starts gained 7.5 percent, following a 5.6 percent rise in December.

Again, permits suggest that housing activity is muted. Housing permits dipped 0.7 percent, following no change in December. The 1.053 million unit pace was up 8.1 percent on a year-ago basis. The market consensus was for a 1.070 million unit pace.

The bottom line is that housing is not adding to economic activity. This means the Fed likely will continue to reinvest mortgage-backed securities to keep rates low. But the long-term trend appears to be that single-family housing is not viewed as strong an investment as in the past.

|

|||||||

| Legal Notices | ©Copyright 1998-2025 Econoday, Inc. |

powered by

![[Apple App Store]](/images/AppleAppStore.png) ![[Econoday on Kindle]](/images/kindle.jpg)

|

||||||